This article is informational only. Tax law is specific to your situation, changes year to year, and the difference between a deduction the IRS accepts and one it disallows often comes down to documentation. Consult a licensed CPA or enrolled agent before filing. Nothing here is legal or tax advice. With that said — most indie authors leave significant money on the table because they don't know what's deductible, how to document it, or how the IRS treats writing income. This guide is the practical orientation that helps you ask better questions when you talk to your tax professional.

The First Question: Hobby or Business?

The single most important tax distinction for an indie author is whether the IRS classifies your writing as a business (Schedule C) or a hobby. The difference is large.

A business can deduct expenses against revenue, carry losses to offset other income, and build legitimate write-offs across years. A hobby — under post-2017 rules — cannot deduct expenses at all. Hobby income is fully taxable. Hobby expenses are not deductible.

The IRS uses a multi-factor test, but in plain language they look at:

- Whether you are operating in a businesslike manner (separate bank account, real recordkeeping, business plan)

- Whether you have made profit in 3 of the last 5 years (the safe-harbor rule)

- Whether your time and effort suggest you intend to make profit

- Whether you depend on the income or treat it as financially serious

- Whether losses are due to circumstances beyond your control or normal startup phase

Most serious indie authors qualify as a business if they keep proper records and operate with intent to profit, even at a loss. New authors get a few years of legitimate startup losses before the IRS pushes back. The single best move you can make in your first year of writing income is to open a separate bank account and credit card for author expenses — that one act establishes "businesslike manner" better than almost anything else.

Read the IRS guidance directly at irs.gov/businesses/small-businesses-self-employed/business-or-hobby.

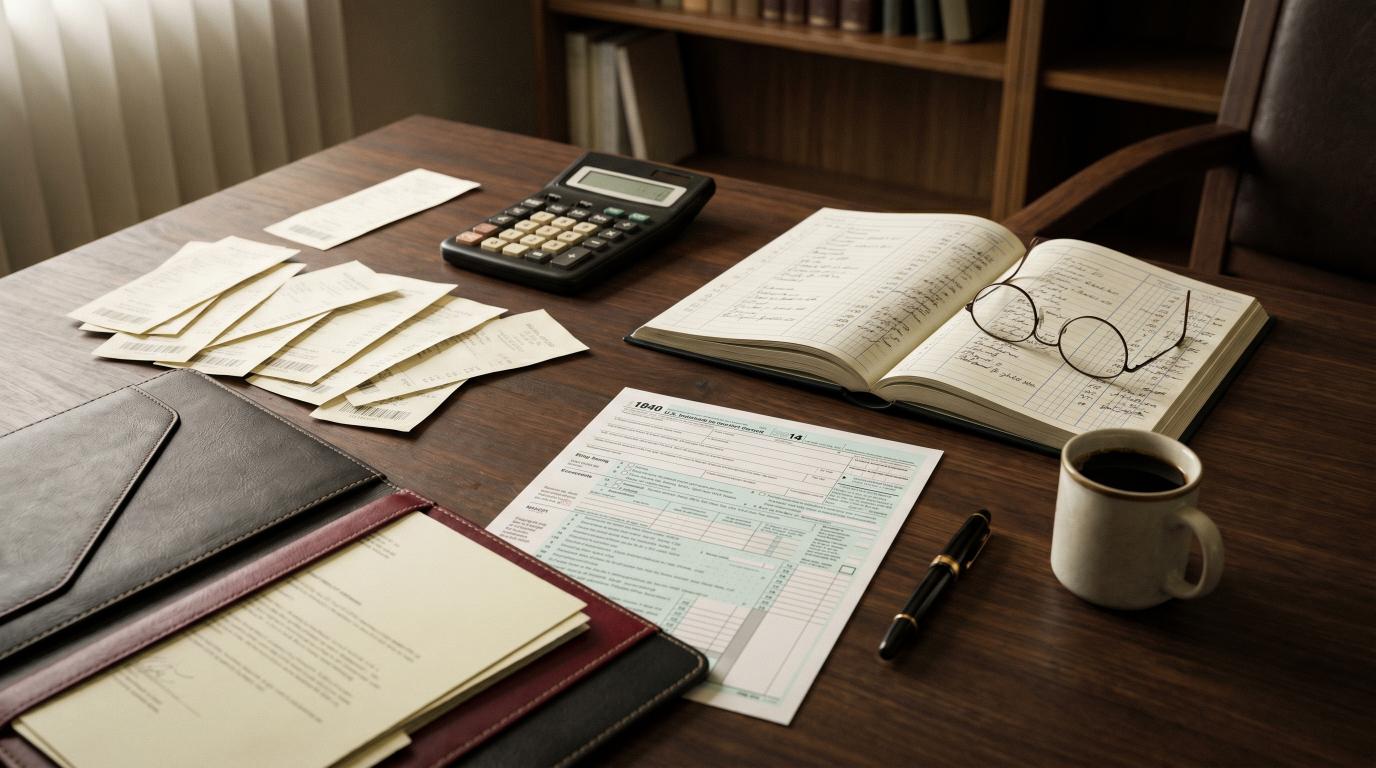

Schedule C — The Form Where Your Author Business Lives

US-based sole proprietor authors report writing income and expenses on Schedule C (Form 1040). Most indie authors are sole proprietors by default — meaning if you haven't formed an LLC or S-corp, you are one already. Schedule C captures gross income (book sales, speaking fees, consulting income, course sales tied to your author work) minus deductible expenses, and the net flows through to your personal 1040.

The key Schedule C lines for authors:

- Line 1: Gross receipts — every dollar of book royalties, speaking fees, course income, paid newsletter income, and ad revenue from your platform

- Line 8: Advertising — Amazon ads, Facebook ads, BookBub Featured Deals, Google ads, podcast sponsorships

- Line 11: Contract labor — payments to editors, cover designers, illustrators, virtual assistants, and contractors. Issue 1099-NEC for any US contractor paid $600+ in the year.

- Line 13: Depreciation — for equipment over a certain threshold; most authors expense laptops directly under Section 179

- Line 17: Legal and professional services — your CPA, attorney, agent, contract review fees

- Line 20: Rent — co-working space, studio rental

- Line 22: Supplies — office supplies, business supplies tied to writing

- Line 24: Travel and meals — book tour travel, conference travel, research trips (with the right documentation)

- Line 27: Other expenses — the catch-all for ISBNs, ISBN agency fees, paid review services, software subscriptions, ARC printing, sample copies sent to reviewers

Each line has rules. The categories matter less than the documentation — a deduction without a receipt or contemporaneous record is hard to defend.

Deductions Most Indie Authors Miss

After working with a lot of authors and reviewing the deductions they typically claim versus the ones they could legitimately claim, these are the most commonly missed.

Editing, cover design, formatting, ISBN

If your book is the product of your business, every dollar you spend producing it is a deductible business expense in the year paid. Developmental editing, copyediting, proofreading, cover design, interior formatting, ISBN purchase from Bowker (or Canadian/UK equivalents for those markets), barcode generation — all deductible.

Marketing, PR, and advertising

Every form of book marketing is generally deductible: Amazon ads, Facebook ads, Goodreads ads, BookBub deals, Kirkus reviews paid submissions, NetGalley listings, editorial press placements through marketing-first publishers like VUGA, publicist retainers, podcast tour booking services. The IRS draws a distinction between ordinary-and-necessary advertising (deductible) and goodwill spending (sometimes not), but ordinary book promotion clearly qualifies.

Software subscriptions

Scrivener, Vellum, ProWritingAid, Grammarly, Plottr, Atticus, Canva Pro, ConvertKit, MailerLite, Notion, Dropbox, Google Workspace, Adobe — any tool you use for your writing or your book business. Deductible. Save the email receipts; most software bills annually with a clear receipt.

Home office

If you have a space in your home used regularly and exclusively for your writing business — not the kitchen table where you also eat dinner — you can deduct a portion of rent, mortgage interest, utilities, internet, homeowners insurance, and repairs proportional to the home office's square footage relative to the home.

The IRS offers two methods:

- Simplified method: $5 per square foot up to 300 square feet ($1,500 max). Easy. Lower deduction for many authors.

- Regular method: actual expenses prorated by the office's share of total home square footage. Often produces a larger deduction but requires more documentation.

The "regular and exclusive" test is real. A spare bedroom that doubles as a guest room fails the exclusivity test. A dedicated office with a desk, bookshelves, and computer that is used only for your writing work passes.

Mileage to author events

Driving to your launch events, signings, school visits, conferences, library talks, podcast recording locations, bookstore meet-and-greets — all deductible at the IRS standard mileage rate (currently in the high 60s of cents per mile; check IRS.gov for the 2026 rate). Keep a contemporaneous mileage log: date, destination, business purpose, miles. An app like MileIQ or a notebook in the glove box both work.

Note: commuting from home to a regular job is not deductible. Driving from your home office to a separate work location for the same business is deductible.

Conferences and continuing education

Writing conferences (Writer's Digest, ThrillerFest, RWA, SCBWI, BookBaby's Independent Publishing conference), craft workshops, masterclasses, business courses tied to your author business — all generally deductible. Keep the registration receipts and a note about the business purpose.

Travel for research

If your novel is set in Lisbon and you take a research trip to Lisbon, the trip can be partially deductible — but only the portion clearly tied to research. Keep notes documenting the research activities, who you met, what you observed. Tacking three vacation days onto a research trip is fine; you just can't deduct those three days of hotel and meals.

Author headshots and branding photography

Professional photography for your author website, book jacket, and press kit is a deductible business expense.

Books you buy in your genre

Genre research is real. Books you buy to study comparable titles, market your work into a genre, or stay current with the field are generally deductible as research/professional development. Keep this reasonable — a $400/year book budget is fine; a $4,000/year book habit will get scrutinized without strong notes.

Subscriptions to industry publications

Publishers Weekly, Writer's Digest, The Hot Sheet, Jane Friedman's Electric Speed, SubStack newsletters about publishing, professional association dues (Authors Guild, SCBWI, RWA, MWA, ITW) — deductible.

What's Generally NOT Deductible

A short list of things authors sometimes try to deduct that don't survive a CPA review:

- Personal clothing (even if you wear it to events) — unless it's branded uniform with logo

- Meals with friends who happen to be authors — unless it's a documented business meal with a clear business purpose

- Books you read for pure entertainment outside your genre

- The full cost of mixed personal/business cell phone plans (only the business portion)

- Vacations vaguely repurposed as "research"

- Expenses without receipts

The IRS standard is "ordinary and necessary." Translate that as: a normal expense in your line of work, that helps you do or grow your business. When in doubt, ask your CPA before you take it.

Quarterly Estimated Taxes

If you owe more than $1,000 in tax for the year on income that wasn't subject to withholding, the IRS expects you to pay quarterly estimated taxes. For most full-time indie authors past their first profitable year, this matters.

The quarterly deadlines are roughly: April 15, June 15, September 15, January 15. Miss them and you may owe an underpayment penalty.

A simple safe harbor: pay either 100% of last year's total tax (110% if your AGI was over $150K) split into four quarterly payments, and you generally avoid the penalty even if you owe more in April. Your CPA can set this up cleanly.

Self-employment tax (Social Security + Medicare, currently 15.3% on net SE income up to the wage base) is the line item most new authors are unprepared for. Plan for roughly 25–35% of net author profit going to combined federal income + SE tax, before any state tax.

When to Form an LLC or S-Corp

For most indie authors with under $50K of net author profit, a sole proprietorship is fine. The added paperwork of an LLC or S-corp doesn't pay for itself.

Around $80K–$120K of net author profit, an S-corp election (made via filing Form 2553 for an LLC or corporation) can start producing real Social Security/Medicare tax savings by separating reasonable salary from distributions. Your CPA will run the math; the savings are typically $3K–$15K/year at those income levels but require a formal payroll setup and additional filings that cost $1.5K–$3K/year to administer.

Don't form an entity for the wrong reasons (it doesn't typically reduce audit risk; it doesn't add credibility for indie authors; it adds complexity). Form one when the tax math justifies it or when you specifically want the legal liability separation.

Recordkeeping — The Habit That Saves You Thousands

A clean recordkeeping system in 2026 looks like:

- Separate bank account and credit card for author business — the single most important step

- Accounting software — Wave (free), QuickBooks Self-Employed, FreshBooks, or even a well-organized spreadsheet

- Monthly category review — 30 minutes a month categorizing transactions

- Receipt storage — digital is fine, photographs of paper receipts work, store in a single cloud folder

- Mileage log — app or notebook, contemporaneous (not reconstructed at year-end)

- Annual CPA review — especially in your first profitable year, before bad habits become expensive

Authors who run this system spend 2–4 hours/month and save thousands at tax time relative to authors who shoebox-and-pray every April.

What VUGA Does for Indie Authors (and the Tax-Adjacent Note)

VUGA Publishing is a marketing-first independent publisher. Our author packages — from the $97 trial pickup through the $14,997 Authority and $19,997 TIME + Rolling Stone tiers — are book marketing expenses. For authors operating their writing as a business under Schedule C, the packages are typically deductible as advertising or marketing expenses in the year paid (consult your CPA for your specific situation).

If you've been on the fence about investing in a press campaign for your book, the after-tax cost is often meaningfully lower than the sticker price suggests. To talk through which package fits your book, contact us. For broader context on the press cost landscape and how editorial features compare to other marketing channels, see book PR cost, the for authors overview, and the editorial network page.

Final Reality Check

Indie author taxes are not as scary as they look once you have the framework. The main moves:

- Treat your writing like a business: separate accounts, real records, businesslike intent

- Deduct what you legitimately can — most authors miss thousands in legitimate deductions

- Don't deduct what you legitimately can't — keep your CPA happy and your audit risk low

- Pay quarterly if you owe meaningfully

- Get a CPA familiar with creative-industry clients in your first profitable year

This guide is a starting framework, not a substitute for the professional advice your specific situation deserves. If you're running real author income, a one-hour consultation with a CPA who works with authors and creatives is one of the highest-ROI hours you'll spend all year.

For US tax authority directly: IRS.gov small business and self-employed center and Schedule C instructions.

Sources for this article: